In the upside-down world, a weak economy is great for Canadian home prices — and people are betting on it. The majority of mortgage debt issued in August has a variable interest rate. This is when a borrower’s interest paid is attached to market rates, as opposed to a fixed rate. Experts, including the central bank, are warning rates will begin to make a sharp rise next year. Whether homeowners realize it, they’re betting experts are wrong about the recovery.

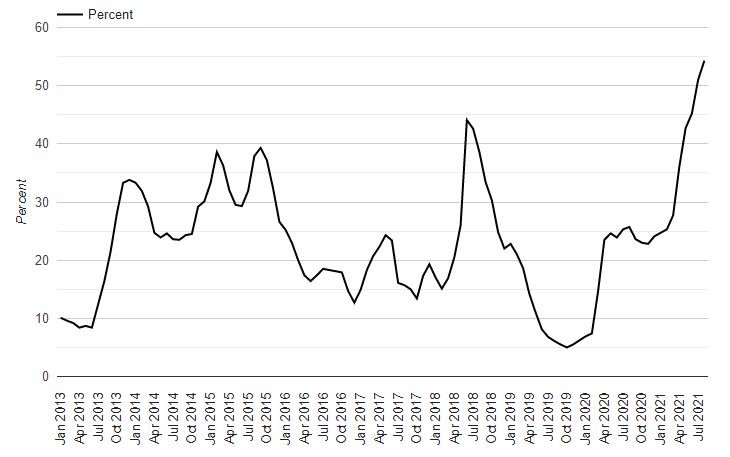

More Than Half Of Canadian Mortgage Debt Issued Is Variable Rate

The majority of mortgage debt lenders have issued, have variable interest rates. The value of the segment reached $24.6 billion in August. This represents 54.3% of funds lenders delivered to mortgage borrowers that month. A year prior, the share of variable rate debt was about half that, so this is a huge surge in popularity. People usually opt for the predictability of fixed rates.

Canadian Variable-Rate Mortgage Market Share

The share of monthly mortgage debt issued by Canadian lenders with variable interest rates. Share is measured in dollar volume.

Source: Bank of Canada; Better Dwelling.

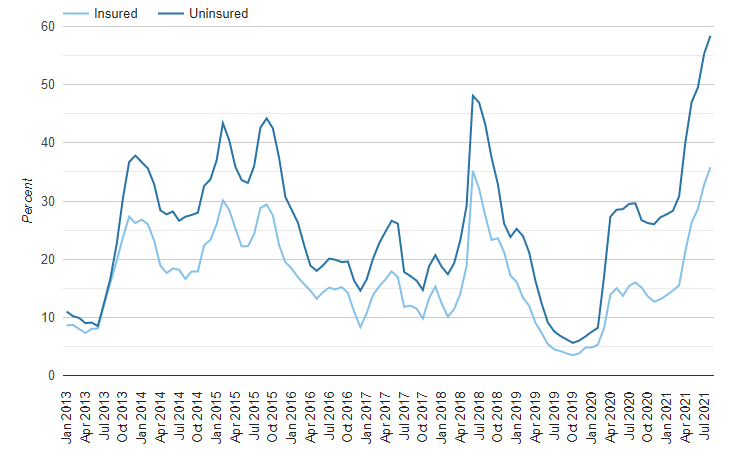

Over 58% Of Uninsured Mortgage Debt Issued Was Variable Rate

Uninsured mortgage borrowers did most of the variable rate borrowing. There was $21.6 billion in uninsured variable-rate mortgage debt issued in August. This works out to 58.4% of all uninsured mortgage debt issued that month. Variable-rate mortgages only had half the market share a year before. Prior to the pandemic, it wasn’t even a double-digit market segment.

Canadian Variable-Rate Mortgage Market Share

The share of monthly mortgage debt issued by Canadian lenders with variable interest rates. Share is measured in dollar volume.

Source: Bank of Canada; Better Dwelling.

Insured Mortgages Are Still Mostly On Fixed Terms

Insured mortgages were the remaining share of variable rate mortgage debt. The segment represented $3.0 billion in August, about 35.8% of the insured mortgage debt issued in the month. A year ago the share was just under half of that (16.0%) and prior to the pandemic, it wasn’t even a double-digit market share.

Why are variable rate mortgages so popular? They’re about 75 basis points cheaper than a 5-year fixed mortgage rate. This is huge savings, and borrowers don’t see variable rates rising fast enough to wipe out those savings. Experts warn variable rate mortgages can rise very quickly next year, doing exactly that. One of those experts is the Bank of Canada.

The economy would need to weaken and inflation would need to fall to avoid a rise in variable interest costs. There’s so much moral hazard right now, homeowners are betting on a weak economy because they think it’s good for them. Mom & pop became Wall Street right before the Great Recession. The economy might get hurt but that would be a net benefit for their assets. Maybe a nuclear disaster or climate collapse will happen. Then home prices can triple.

Borrowers are stress-tested, so the fear of rising defaults due to a jump in interest costs is unlikely. The macro concern is mostly related to the shift in consumer spending in the rest of the economy. Just because you can afford to pay more for your mortgage, doesn’t mean it’s a good thing for the economy. The money diverted to paying mortgage debt comes from consumer spending and investments.

Courtesy: betterdwelling.com

Posted by Teri-Lynn Jones on

Leave A Comment