Canada’s oldest bank has a warning for homebuyers — prices don’t always rise. The uncharacteristic message came from BMO‘s chief economist Douglas Porter. Canada has seen few home price corrections, causing homebuyers to think of it as “risk-free.” Not just in Toronto or Vancouver, but virtually every market in the country, all simultaneously. BMO wants you to know that’s not always the case, and risks rise the longer home prices avoid a correction.

Canadian Real Estate Prices Climbed Despite A Decade Of Warnings

Canadian real estate has faced “bubble” warnings for nearly a decade that have not come true. Some dudes named Poloz and Macklem were even ranting about it back in 2013 but have since come around. Justified or not, listening to warnings for a decade tends to desensitize people. BMO argues this can’t go on forever, especially with the recent movements intensifying.

Oxford Economics, a global macro research firm, had a similar warning. They cited it as a potential example of positive duration dependence. This economic concept states that risk rises the longer it’s absent.

“There is a sense among some that the Canadian housing market can never falter. After all, in the face of more than a decade’s worth of dire warnings, prices have mostly climbed relentlessly,” said Porter.

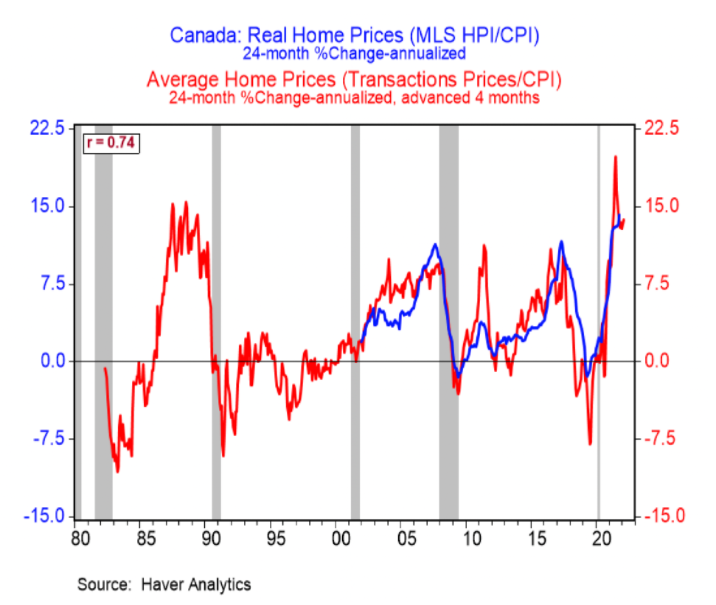

Canadian Real Estate Has Only Had Two Major Stumbles

Canadian real estate has only experienced a limited number of corrections since 2000. Just two, to be more precise. There was the 2008/09 cycle during the global financial crisis. Then there was the foreign buyer mini-bubble in 2017/2018. The central bank had also begun to raise rates during the latter, cooling price growth. Vast injections of mortgage credit reversed both slow periods. Flooding the market with credit only extends market inefficiencies though, turning a minor issue into a big one.

“Looking back to the start of the century, the market has had only two brief stumbles, even after adjusting for inflation,” he said. “… But, realistically, it’s mostly been a one-way trip north for the past 20 years.”

Canadian Home Prices Can’t Rise Always And Everywhere Forever

Great, that means party on? Not exactly. The bank warns that this hasn’t always been the case, and the corrections have been rough. “Note the two brutal corrections in the early 1980s and then again through the first half of the 1990s. In fact, had you bought a home in 1989, your investment would still have been down in inflation-adjusted terms 15 long years later,” he adds.

According to the bank, Canadian home prices had only recovered from the late 1980s bubble in 2004. Some experts warned that the US housing crash would spill over. However, Canadian home prices had only made modest gains by then, compared to the late 80s peak.

Toronto real estate also charted a similar path, but it took much longer to recover. The city's home prices didn't overtake its 1989-inflation adjusted peak until 2011. When experts like Macklem had warned, they hadn’t taken inflation into account. Which seems fitting in hindsight, doesn’t it?

No, BMO isn’t calling an epic crash that blows up the global economy in the next few months. “To be clear, we are not in the ‘deep correction’ camp, but we are in the camp that believes housing does not always and everywhere rise in value,” he said.

The bank sent a similar message earlier this year - once again — warning, but not calling a housing crash. Instead, they suggest make sure you like the place you buy because buying in a "bubble" means you can be stuck with it for a while. After all, no one wants to do hard time in a 400 sqft box for 15 to 20 years because the mortgage was a steal.

Courtesy: betterdwelling.com

Leave A Comment